What is the 50/30/20 Rule of Budgeting?

Topics Covered

What is the 50-30-20 Budget rule?

How to apply the 50-30-20 rule?

Conclusion

The 50-30-20 budgeting rule is one of the most popular and easily understood budgeting techniques, which is clear and intuitive. The rule was popularized by United State Senator Elizabeth Warren in her book. All your worth: The Ultimate Lifetime Money Plan. So What is a 50-30-20 budget?

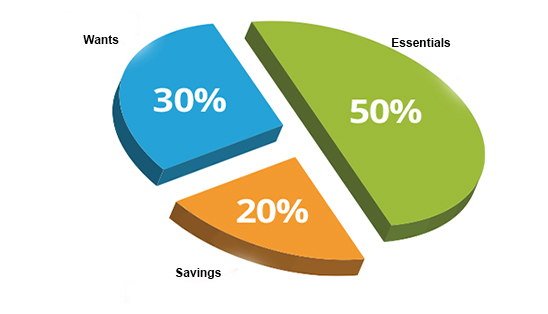

It’s a simple rule that asks an individual to allocate his after-tax income into three components: 50% on needs, 30% on wants, and 20% on savings. The beauty of the rule being is it’s simple to understand and easy to follow, allowing every individual to save a constant percentage of their income every month.

What is the 50-30-20 budget rule?

As stated earlier, the 50-30-20 rule helps individuals keep tabs on their expenses, especially if they struggle with saving money at the end of every month. The rule is direct where it expects individuals to divide their expenses across three broad categories:

1. 50% Needs

Needs are the expenses that are necessary for an individual’s survival. Thus according to the 50-30-20 rule, 50% of the individual’s income can be spent on his needs. These include expenses such as:

Rent

Utilities such as Electricity, Water bills

Transportation Cost

Groceries

House of car EMIs

Children’s Education

Insurance Expenses

Needs should only include expenses that sustain a basic standard of living with all your obligations taken care of these do not include eating out, entertainment expenses, lifestyles expenses etc,

But there is always a possibility that an individual’s needs can account for more than 50% of his income. Though this is undesirable, this leaves an individual with a few options to cut back on luxuries, look to increase his income or look for alternatives where he may have to downsize his current lifestyle.

2. 30% on Wants

For an individual, wants are all the expenses he makes that are unnecessary for his survival and can be considered the luxuries of life. Wants include all the expenses that add spice to individual life and make it more enjoyable. Wants expenses can be any of the following:

Entertainment Expenses like movies or Netflix

Dining Out

Gym Membership

Shopping

Holidays

Wants can also include expenses where an individual chooses to spend on items that have a cheaper alternative like buying luxury watches over traditional watches or spending on SUV over buying sedans. If an individual finds he is spending more than 30% of his income on wants he can look for expenses to cut back and does not ask you to stop enjoying your life by spending on items that give you joy. But it’s a tool that gives an individual a choice to watch over his spending habits and be the one in control.

3. 20% on Savings

While Needs and Wants take care of your present self, The money within this category takes care of your future self. All the money saved within this category ensures that the future self is looked after if he does not have a job or gets sick. This allows him to enjoy the same level of lifestyle he may be currently living. Saving can include:

Emergency Funds

Tax Saving Funds like Provident Funds, NPS, ELSS

Mutual Funds or Stocks

Loan Prepayment i.e money more than your monthly EMI

Saving helps an individual with his long-term goals like buying his house, marriage expenses, retirement funds, children’s college education, etc

How to apply the 50-30-20 rule?

While we understand the 50-30-20 rule, how do we apply the same to our life?

1.Calculate your after-tax income

For a self-employed professional, you would need to calculate your last month, income and deduct all the business expenses and taxes. For salaried professionals, account for your monthly income and add the deductions for pension Funds, EPF, and Health insurance back to the salary.

2.Track last month’s expenses

You would need to account for all your expenses over previous months and group them across broad categories like Rent, Utilities, Groceries, Leisure and Entertainment, etc. You could use Excel or Budgets Apps to track the same.

Then based on the three categories, you would need to divide them across Needs, Wants, and Saving. A few things which need to be kept in mind are if these expenses are optional; If yes, then they ate Luxuries. Additionally, For expenses such as loans, while the EMI is taken to be part of needs, Any loan repayment is taken as savings. Even retirement funds are a part of this saving category.

3.Evaluation

You would need to assess how much you spend across the three categories. If your Luxuries are more than 30%, you might shift those funds to savings, or if your needs are below 50% and your saving goals are being met, maybe it is time for a vacation.

Conclusion

The 50-30-20 rule for every individual should be taken as a foundation or starting point to manage their budgets. When individuals struggle to keep their budget in check, this rule allows them to keep track of their expenses, enabling a person to save for a rainy day fund, take care of unexpected expenses and save for retirement.

Thus, if an individual is to follow a 50-30-20 budget, he can be expected to live a comfortable life where his expenses are covered, his future is secured, and he has room to spend on the Luxuries that make the life worth living.